Generative AI in finance: production use cases and what's actually shipping

Where GenAI is genuinely cutting cost and improving customer experience in finance today — seven production use cases with real deployment examples, the implementation challenges, and the CFO playbook.

McKinsey projects $200B–$340B in annual GenAI value capture for the banking sector — primarily through productivity gains. The number is real; the question is whether your finance organization can capture its share. Most CFOs are getting GenAI scoping wrong: optimizing for impressive demos rather than measurable workflow improvements, rushing to ship without compliance discipline, or waiting indefinitely for "perfect" technology that doesn't exist.

This article maps seven GenAI use cases that are genuinely shipping in financial services today — with real deployment examples, the architectural patterns we see succeed, and a CFO playbook for getting the investment right. For deeper treatment of banking-specific GenAI, see our companion GenAI in banking article. For the production reference architecture in regulated finance, see /fintech/rag.

What GenAI is actually doing in finance today

The honest framing: GenAI in finance is mostly augmenting humans, not replacing them. End-to-end autonomous workflows — discovering trends, devising strategy, and executing autonomously — aren't production-ready in 2026. Wide-scale autonomous deployment is constrained by data privacy, fiduciary duty, and the regulatory load on financial institutions. What ships is GenAI as copilot: faster analysis, better personalization, more efficient operations, with humans in the decision loop.

The four concrete benefits we see in production deployments:

- Lower costs. MIT/UBS research frames GenAI's primary financial-sector value as cost reduction — most of it from automating manual tasks and freeing employees for higher-value work.

- Higher productivity. Accenture estimates LLMs could affect 90% of working hours in banking. BCG reports productivity gains of up to 20% at companies deploying GenAI.

- Better customer experience. Personalization at scale — investment advice, financial guidance, faster customer service. Magnifi's investment platform uses ChatGPT for personalized portfolio mentoring as one example.

- Better risk management. Loan applicant analysis, fraud detection, market scenario simulation — areas where GenAI extends classical risk models with unstructured-data reasoning.

Seven production use cases

Where GenAI is genuinely working in financial services today, with public reference deployments.

1. Financial reporting, summarization, document analysis

GenAI drafts financial reports — statements, budgets, risk reports, compliance reports — that humans review and adjust. Summarizes large document sets. Answers questions from extensive financial knowledge bases.

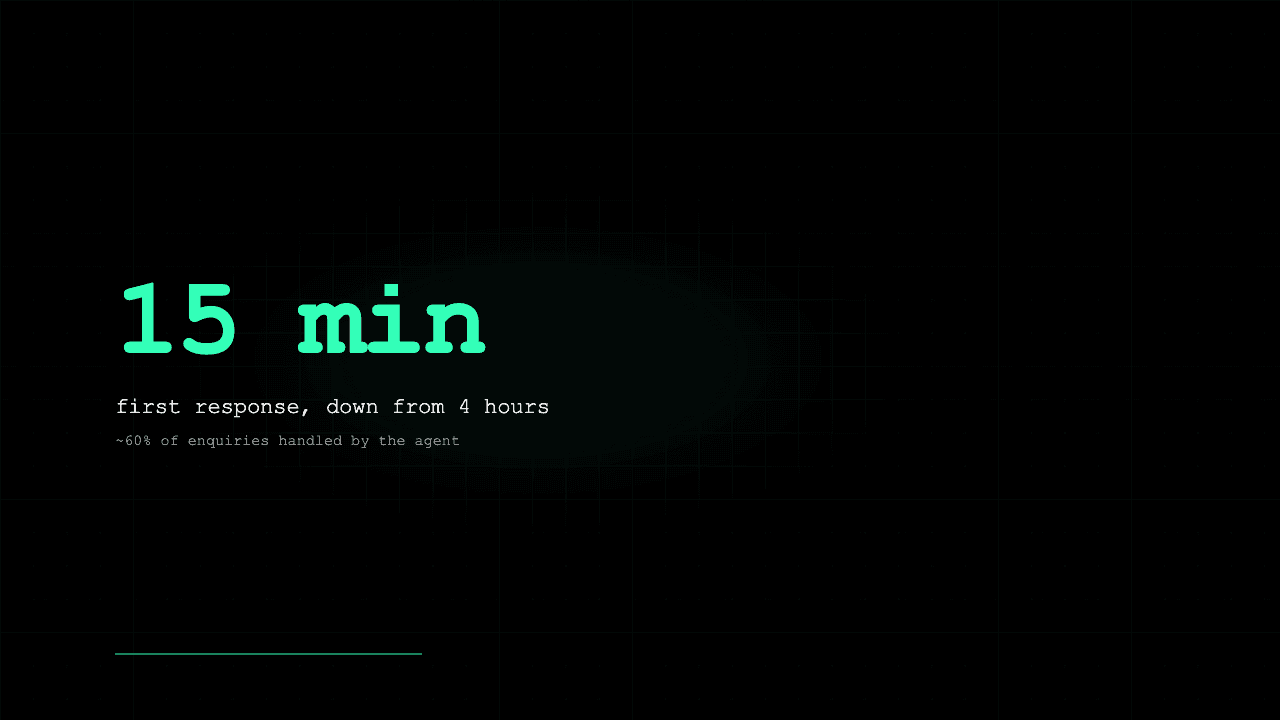

Reference deployment: Cyber insurance firm Cowbell deployed MooGPT, a tool that searches the firm's financial knowledge base and provides real-time short answers to insurance agents during policyholder calls. The pattern: domain-specific RAG over internal documentation, optimized for low-latency Q&A.

2. Personalized financial recommendations

Customer segmentation by financial status and demographics. Tailored recommendations per cohort. Investment portfolio construction. News-impact analysis on asset pricing.

Reference deployment: JPMorgan is developing IndexGPT, a GenAI bot for customized investment advice — analyzing financial data and selecting securities tailored to individual customers and their risk tolerance. The architectural pattern: the model never makes the actual investment decision; it surfaces options for human advisors or customers to choose from.

3. Internal copilots for high-skill professionals

Goldman Sachs is using GenAI to assist programmers — reporting 20–40% productivity gains in software development. KPMG deployed ChatGPT (running inside the firm's firewall) for tax consultants, expecting up to $12B in revenue from related initiatives.

The pattern: GenAI as a productivity multiplier for already-expensive professionals. The ROI math is straightforward — if a $200K tax consultant becomes 20% more productive with a GenAI copilot, the copilot pays back its build cost in the first quarter of deployment.

4. Defense against financial crime

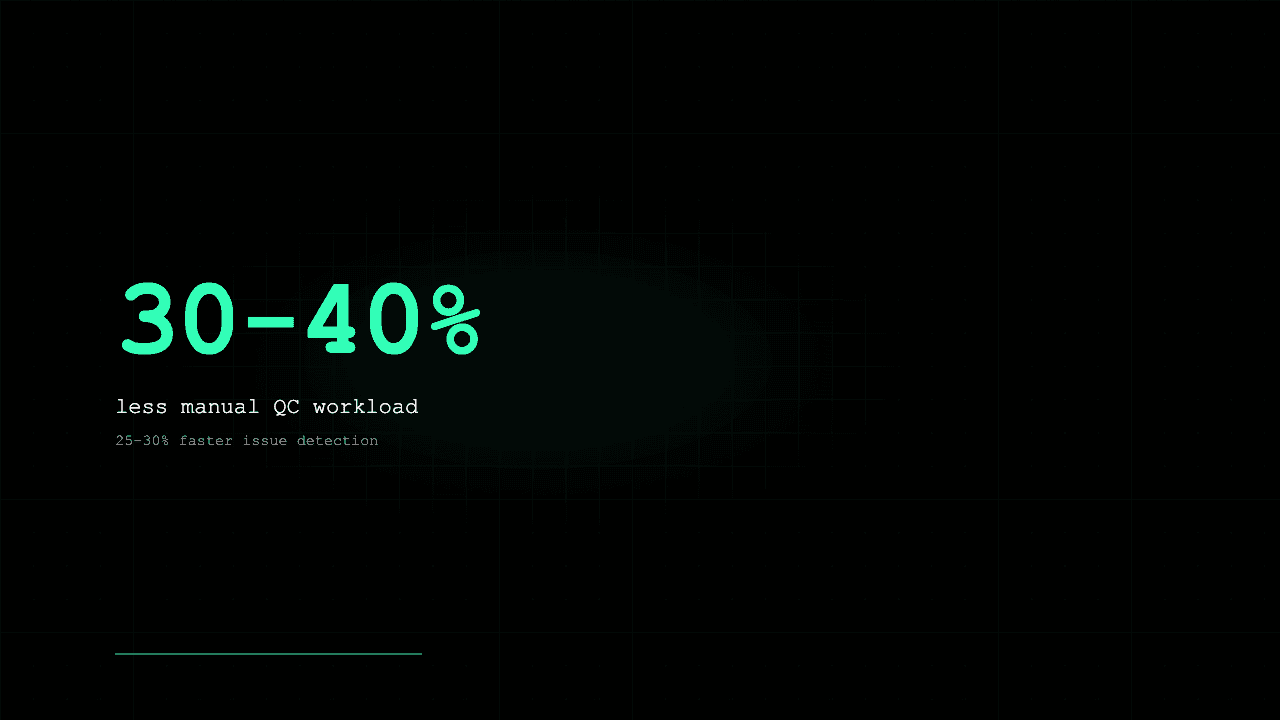

NICE Actimize built a GenAI-powered tool for financial crime investigation — analyzing and summarizing data, issuing alerts, generating reports. The company reports 50% reduction in investigation time, 70% reduction on Suspicious Activity Report (SAR) filing.

The architectural pattern: GenAI for unstructured data feature extraction (transaction narratives, customer correspondence, external data) feeding into traditional fraud scoring models — keeping the actual decision in explainable territory required by regulators.

5. Market intelligence

LLMs crawl internet, social media, internal data sources for market insights — demand shifts, competitive intelligence, sentiment trends. Morgan Stanley's Wealth Management department deploys OpenAI to mine proprietary data. BloombergGPT — a 50B-parameter model trained on 700B tokens of financial data — provides searchable summaries and insights from Bloomberg's data corpus.

Also: market scenario simulation, outcome prediction, and portfolio impact modeling. The pattern: GenAI generates the analytical surface; humans pick the scenarios and act on the insights.

6. Contract generation and management

Specialized GenAI fine-tuned on legal language drafts contracts, articulates non-standard terms, compares clauses, generates negotiation arguments.

Reference deployment: BNY Mellon partnered with an AI vendor to customize a GenAI model that streamlines custodial agreements — drafting customized agreements, routing them to stakeholders, alerting on non-standard clauses or missing details. Heavy compliance review before drafts reach customers.

7. Anomaly and fraud detection

Per a 2023 KPMG survey, fraud detection is the top GenAI application in finance — 76% of respondents identifying it as a key use case. Real-time transaction monitoring, behavioral anomaly detection, complex fraud scheme identification.

Reference deployment: Stripe uses GPT-4 to identify malicious actors on its community forum — flagging questionable accounts and notifying the fraud team for investigation. The pattern that ships: GenAI for unstructured data classification + human review for action.

Why GenAI in finance is harder than in other industries

Five challenges that consistently slow GenAI deployment in financial services.

Legacy technology. COBOL still supports 80% of credit card activity and 85% of ATM transactions. Old programming languages, isolated data silos, proprietary message formats — all of which add 30–50% to GenAI integration cost. Counter-intuitively, GenAI itself increasingly assists in legacy modernization, generating modern equivalents of legacy logic.

Talent shortage. GenAI engineering talent with financial domain knowledge is among the scarcest hires in tech. Most financial institutions use external delivery teams during the build phase, with knowledge transfer to internal teams during operation.

Bias and explainability. GenAI models inherit training-data bias. Financial applications — credit decisions, lending, investment recommendations — are subject to fair lending laws (ECOA, GDPR Article 22). Black-box models that can't explain their reasoning don't pass compliance review. The fix: RAG with span-level citations, output-level explainability layers, continuous fairness monitoring across protected classes.

Hallucination. Financial advisors with hallucinating GenAI tools have a competence problem; financial institutions with hallucinating customer-facing GenAI have a regulatory problem. Mitigation: RAG grounding plus refusal templates that prefer "I don't know" over confident-incorrect.

Intellectual property and regulatory uncertainty. Training data licensing, output IP rights, market manipulation risks, fiduciary duty concerns — all areas where regulatory clarity is still emerging. The pragmatic path: deploy where regulatory pathway is clear; pilot where it's emerging; wait where it's contested.

For deeper treatment of these failure modes specifically in fintech RAG architecture, see our 10 RAG architecture mistakes article.

CFO playbook for GenAI implementation

Six practical steps from a real CFO scoping conversation:

1. Pick the right use cases

Start with two or three workflows that have measurable financial impact, manageable complexity, and stakeholder buy-in. Don't deploy GenAI just because the technology is interesting. If a less expensive technology (fixed rules, classical ML, off-the-shelf SaaS) solves the workload adequately, ship that instead. The discipline to say no to inappropriate GenAI scope saves more capital than any other single decision.

2. Decide build vs buy

Building a foundation model from scratch isn't realistic for most financial institutions — the cost economics don't pencil out. Four practical paths:

- Open-source as-is. Llama, Mistral on customer infrastructure. Initial setup $30K–$80K plus ongoing operational cost.

- Open-source fine-tuned. Customized for domain. $100K–$250K initial. Best when residency or regulatory requirements rule out hosted models.

- Commercial API as-is. Claude, GPT, Gemini direct. Pay per query, no infrastructure. Fastest to ship, vendor lock-in trade-off.

- Commercial fine-tuned. Vendor-managed fine-tuning of hosted models. $25K–$80K. Domain accuracy without infrastructure burden.

For most financial institutions, the right starting point is commercial API + RAG, with migration to fine-tuned or self-hosted as scale and compliance requirements demand.

3. Safeguard against bias and adversarial misuse

After deployment, ongoing fairness audits across protected attributes. Validate that the model doesn't infer protected attributes from non-protected features. Test for adversarial misuse — can the model be exploited via prompt injection, jailbreaking, or output manipulation. Continuous monitoring, not one-time validation.

4. Encourage AI engineer + end-user collaboration

Involve end users (advisors, analysts, fraud investigators, tax consultants) in model training and customization. Their feedback drives meaningful refinement. Their adoption drives ROI realization. Engineering-only GenAI projects routinely under-deliver on real-world value because the engineers don't know which workflow improvements actually matter to operators.

5. Prepare the workforce

Skills gap analysis. Reskilling and upskilling programs for existing employees. Selective hiring of GenAI talent where in-house capability is critical. Partner with delivery teams for build phase if you don't want to absorb senior AI engineering hiring overhead during the steady-state operating phase.

6. Establish responsible AI governance framework

PayPal's responsible AI framework is a useful reference — explicit accountability mechanisms, policies, and ethics; specific guidelines for employees using models in different settings; control mechanisms (kill switches for production disruptions); HITL approval gates for high-stakes outputs; documentation of training data with consent and right-to-be-forgotten provisions.

What's deployable today vs what's still pilot

Honest framing for CFOs weighing investment.

Production-ready:

- Internal knowledge assistance (advisor copilots, tax consultants, ops staff)

- Document processing and contract drafting (with human review)

- Fraud detection feature extraction (feeding into explainable scoring models)

- Customer service automation for routine queries

- Regulatory compliance documentation drafting

- Code generation assistance for engineering teams

Pilot-stage:

- Customer-facing investment advice without advisor oversight (fiduciary risk)

- Autonomous credit decisioning (HITL still required)

- Algorithmic trading driven by GenAI reasoning (regulatory clarity emerging)

- Fully autonomous fraud or AML decisions

Wait:

- Cross-border deployments where regulatory regimes conflict

- GenAI for systemically important decisions (capital allocation, stress testing) where regulator acceptance is still developing

- Multi-modal financial applications combining vision, text, and structured data for high-stakes regulated workflows

The principle: GenAI ships in finance when it augments human judgment with grounded, auditable, explainable outputs. It stalls when it tries to replace human decision-making in regulated processes.

To sum it up

The competitive context is real. Mike Mayo of Wells Fargo described the future state as "every employee with an AI copilot or AI coworker, every customer with the equivalent of an AI agent." We're not there yet. But the financial institutions deploying GenAI thoughtfully today — with compliance discipline, with focused workflow scope, with the right architectural patterns — are building the operational moat that will compound for years.

The capital required is bounded. The use cases are clear. The patterns that work are documented. What's missing in most financial GenAI initiatives isn't budget or technology — it's the scoping discipline to pick the right workflows, the governance discipline to ship safely, and the operating discipline to scale on validated outcomes rather than enthusiasm.

Ready to scope a GenAI investment for your finance organization? Run the Project Estimator for a deterministic ballpark across implementation paths, or book a 45-minute Discovery with our GenAI engineers — we'll review your data, regulatory constraints, and integration surface and tell you honestly which workflows are ready for GenAI today and which to keep in pilot.

Talk to the team behind this

Building something like this in production?

Our senior engineers ship this kind of work for real teams. 45-minute call, no pitch deck — just architecture, trade-offs, and whether we're the right fit for your problem.