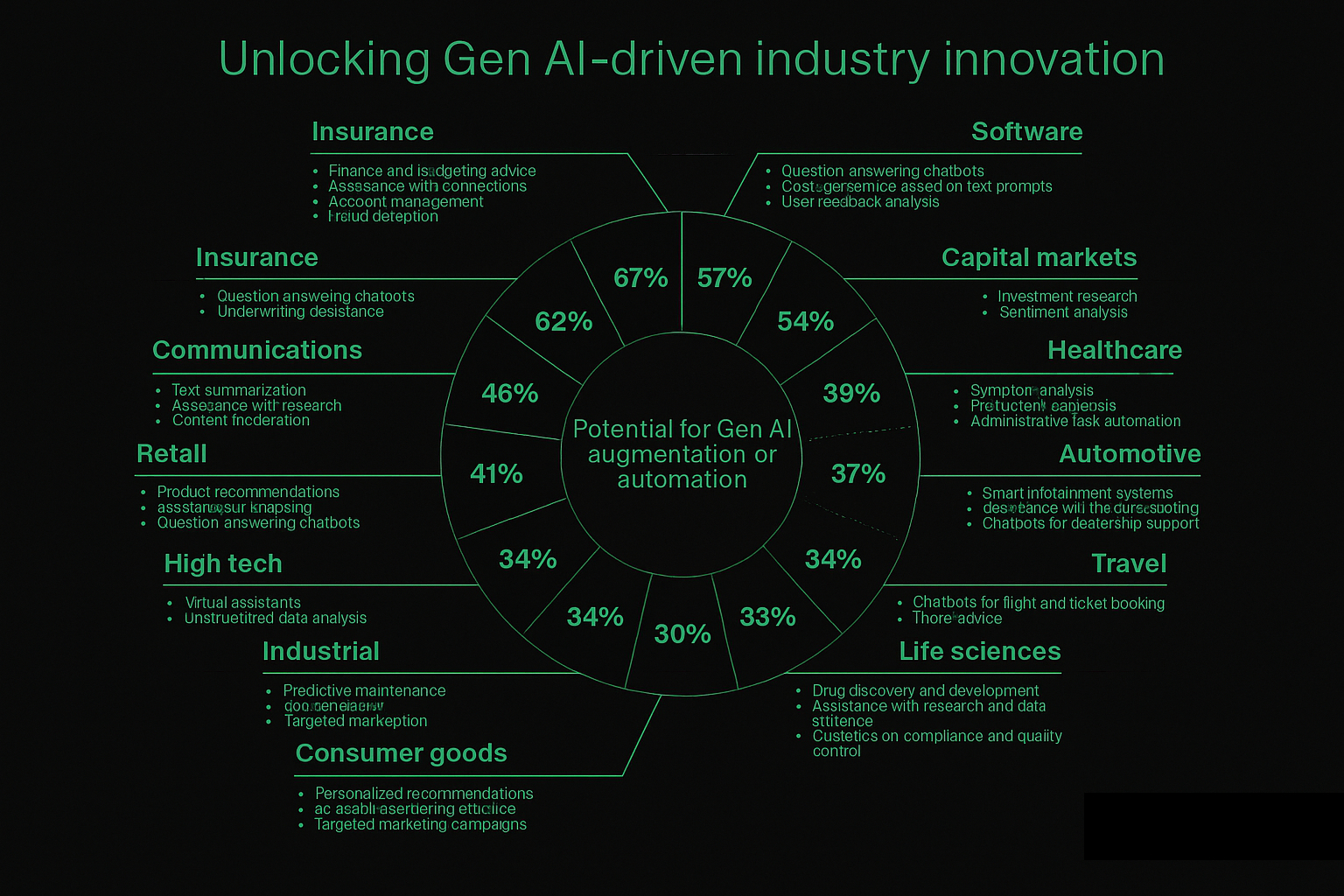

Navigating generative AI trends for C-level executives

Five GenAI trends that actually matter for executive investment decisions in 2026 — multimodal, small language models, autonomous agents, open-vs-proprietary, and tailored solutions. With concrete impact framing for each.

The honest framing for executives reading GenAI trend reports: most trends don't matter for your business this year. The ones that do affect investment decisions deserve careful attention; the rest are vendor noise. This article maps the five trends that genuinely affect executive scoping in 2026 — what they mean, where they ship, and how they should shape capital allocation.

McKinsey estimates GenAI's annual economic impact could surpass $4.4T globally. Foundation models are projected to reach median human performance by end of decade — 40 years ahead of previous predictions. The market opportunity is real, but capturing your share requires executive discipline about which trends to invest in now versus which to monitor.

For deeper engineering treatment of GenAI cost economics across implementation paths, see our calculating the cost of generative AI and evaluating GenAI cost vs value articles.

Five GenAI trends that actually shape executive decisions

Trend 1: Multimodal GenAI is reaching production maturity

GPT-4V, Claude with vision, Gemini 2.5 Pro, and a wave of open-source multimodal models (LLaVA, Qwen-VL) are bringing combined text-image-audio reasoning to deployable production systems. Workloads that previously required separate models for OCR, classification, and generation can now run through a single model with cross-modal context.

Why it matters for executives: workflows involving documents with images (insurance claims, medical records, manufacturing inspection reports), customer interactions across channels (text + voice + visual), and content generation pipelines now have unified architectural options that didn't exist 18 months ago. Integration cost drops significantly when one model handles the full pipeline.

Impact on investment scoping:

- Document processing pipelines that combined OCR + classification + report drafting through 3-4 separate systems can often consolidate to a single multimodal model, cutting integration complexity 40-60%.

- Cross-channel customer experience automation becomes economically viable for mid-size enterprises, not just hyperscalers.

- Manufacturing and field service applications for visual inspection + report generation become significantly more cost-effective.

The trade-off: multimodal models cost 2-4× their unimodal equivalents at the same task. Pencils out when modalities genuinely interact; doesn't when one modality dominates. For deeper treatment, see our understanding multimodal AI systems article.

Trend 2: Small language models shift unit economics

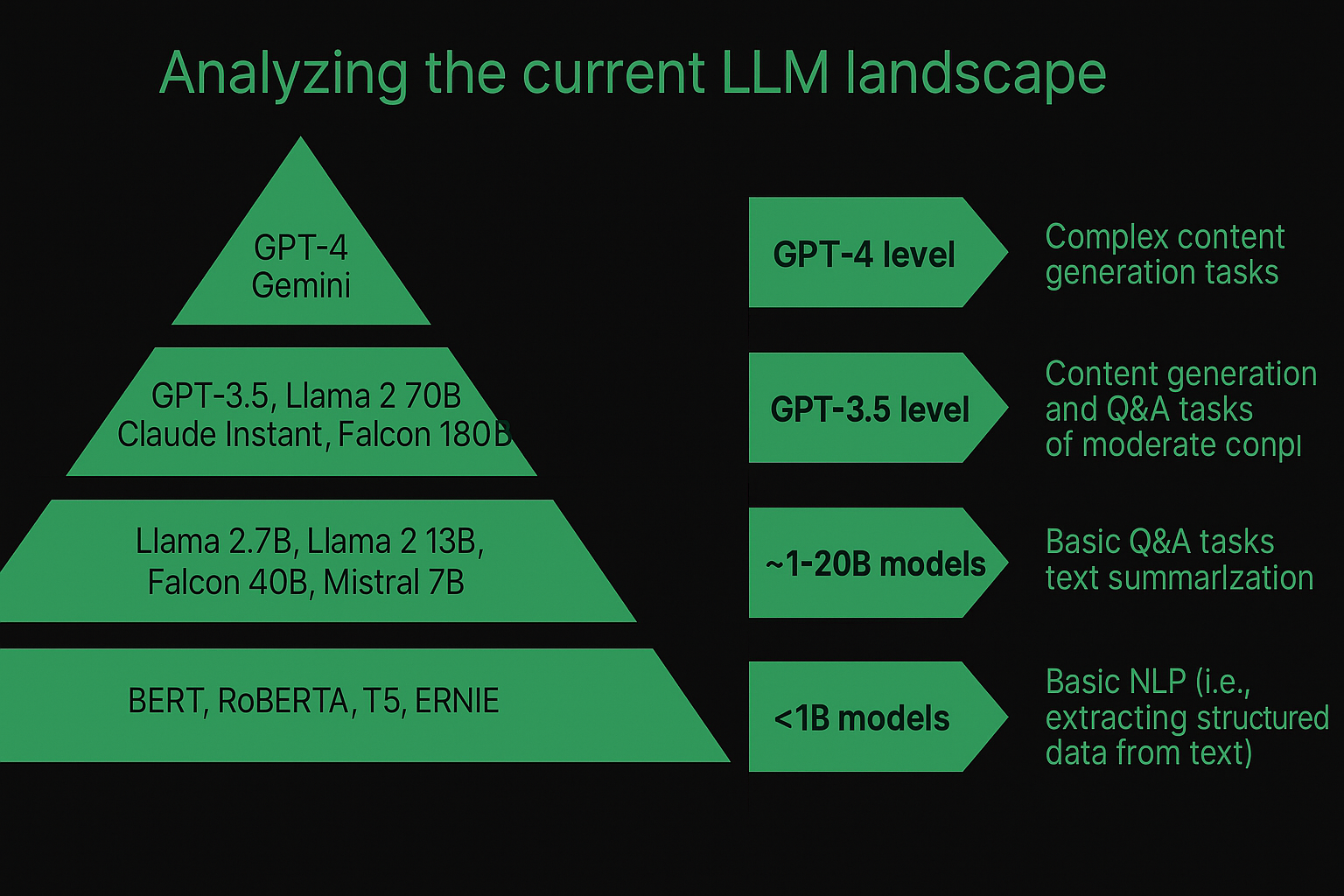

Microsoft Phi-4, Mistral 7B/Ministral, Llama 3.x (1B/3B/8B), Gemma 2 — production-stable open-source SLMs in the 1-13B parameter range are increasingly capable of handling enterprise workloads at a fraction of foundation-model cost.

Why it matters for executives: the cost economics of GenAI deployments shift dramatically when SLMs can replace foundation models on bounded workloads. A 200K-query/month customer support workload runs $2,400/month on Claude Sonnet 4.6, $640/month on Claude Haiku 4.5, and ~$1,500/month amortized on a self-hosted Llama 3.3 8B instance. At enterprise scale (1M+ queries/month), self-hosted SLMs win on unit economics by 50-80%.

Impact on investment scoping:

- Data residency requirements become solvable without sacrificing capability. SLMs running on customer-controlled infrastructure handle workloads that previously required hosted models — particularly important for healthcare (HIPAA), finance (SR 11-7, DORA), government (FedRAMP), and EU deployments under the AI Act.

- High-volume internal workloads should be re-scoped for SLM economics. Customer support, document classification, sentiment analysis, internal knowledge Q&A — all candidates for SLM deployment when traffic crosses 1M+ queries/month.

- Edge deployments expand significantly. SLMs in the 1-3B parameter range deploy on consumer-grade GPUs, enabling on-premises and edge-AI architectures that weren't feasible 18 months ago.

For deeper engineering treatment, see small language models — a smarter way to get started with generative AI.

Trend 3: Autonomous agents move from pilot toward production

The agent ecosystem (LangGraph, CrewAI, AutoGen, native agent capabilities in foundation models) has matured significantly. Agents that plan multi-step work, integrate with business systems, and self-correct on failures are reaching production deployment in narrow workloads — though autonomous agents in regulated workflows still require explicit human-in-the-loop gates.

Why it matters for executives: the gap between "AI as analytic tool" and "AI as autonomous workforce participant" is closing on bounded workflows. Customer service automation, internal knowledge work, document processing, and regulated decision-support workflows are all areas where autonomous agents are shipping today with measurable productivity gains.

Impact on investment scoping:

- Customer service workforce planning should account for agent-driven automation reaching 30-60% deflection rates on routine queries.

- Internal knowledge workflows (HR queries, IT support, financial reporting drafts) can be substantively automated with significant ROI on bounded workloads.

- Regulated workflows require explicit governance design. Healthcare diagnostic support, financial decision-making, legal document drafting — all require HITL gates that constrain agent autonomy.

For deeper architectural treatment, see what are AI agents and how do you implement them and how AI agents transform the healthcare sector. For agent-specific cost framing, see how much does AI agent development cost.

Trend 4: Open-source models close the capability gap

The capability gap between proprietary foundation models (Claude, GPT, Gemini) and open-source alternatives (Llama, Mistral, DeepSeek, Qwen) has narrowed dramatically. On many workloads, open-source models match or exceed proprietary performance — particularly when fine-tuned for domain-specific tasks.

Why it matters for executives: vendor lock-in to proprietary providers becomes increasingly avoidable. Self-hosted open-source models give full control over data, deployment, and cost — at the price of operational complexity. The strategic question is whether your organization wants to own that operational complexity or delegate it to a provider.

Impact on investment scoping:

- Vendor risk mitigation becomes meaningfully achievable. Multi-provider strategies, fallback to open-source alternatives, hybrid deployments combining proprietary and open-source — all viable patterns in 2026.

- Long-term cost optimization improves with open-source. Per-token API pricing scales linearly with usage; self-hosted infrastructure cost scales sublinearly. At scale, the savings compound.

- Geographic and regulatory flexibility improves significantly. Open-source models can be deployed in jurisdictions where hosted providers can't operate.

The trade-off: operational complexity. Hosting, scaling, monitoring, and updating self-hosted models requires real MLOps capability. Most enterprises start with proprietary APIs, validate workloads, and migrate to self-hosted as scale and compliance demands grow. For deeper treatment of LLM training options including open-source fine-tuning, see LLM training: the process, stages, and fine-tuning gritty details.

Trend 5: Industry-specific tailored GenAI solutions emerge

Off-the-shelf foundation models are being joined by industry-tuned alternatives: BloombergGPT for financial services, Hippocratic AI for healthcare, Harvey for legal, Med-PaLM 2 for medical Q&A. These models start with foundation-model capability plus domain-specific fine-tuning, embedded compliance patterns, and pre-built integrations.

Why it matters for executives: the build-vs-buy decision shifts. Where previously every enterprise had to build domain-specific RAG and fine-tuning on top of generic foundation models, increasingly there are pre-built domain-tuned alternatives. The trade-off: customization vs. time-to-deploy.

Impact on investment scoping:

- Re-evaluate "build" scoping in industries with mature tailored solutions. Healthcare diagnostic support, legal research, financial analysis — all have credible pre-built alternatives that can shorten time-to-deployment from quarters to weeks.

- Fine-tuning costs drop when starting from already-domain-tuned models. Less data needed, less training time, shorter validation cycles.

- Vendor evaluation becomes more critical. Industry-tailored solutions are often built by smaller players with limited operational track records. Due diligence on the vendor matters as much as the technology.

For broader cost framing across implementation paths (commercial-as-is, fine-tuned commercial, open-source-as-is, open-source-fine-tuned), see calculating the cost of generative AI.

What to do with these trends

Five concrete actions for executives weighing 2026 GenAI investment:

1. Audit existing AI workloads against the trend implications. Workloads scoped 12+ months ago likely make different architectural sense in 2026. Multimodal consolidation, SLM economics, agent-driven automation, open-source alternatives, and industry-tailored solutions all create re-scoping opportunities.

2. Validate cost assumptions on actual traffic. API economics shift quickly with model selection (Sonnet vs Haiku vs Flash), and self-hosting crossover points depend heavily on workload shape. The cost models from 2024 don't apply in 2026.

3. Plan for regulatory complexity, not capability constraints. Capability is rarely the binding constraint anymore for production deployments. Compliance pathway, data residency, audit trails, and HITL gates are the work that determines whether projects ship.

4. Build operational AI muscle internally or via durable partnerships. The 18-month half-life of frontier models means architectural decisions made in 2026 will need revisiting in 2027. Internal MLOps capability or a durable delivery partnership matters more than picking the "right" model today.

5. Sequence by ROI, not by hype. The trend with the most marketing attention isn't necessarily the trend with the highest ROI for your specific workload. Match trend implications to your actual revenue or cost levers.

Where the trends converge

Looking 18-36 months ahead, four convergence patterns matter for long-term planning:

Hybrid agent + multimodal + SLM architectures. Production deployments combining autonomous agent reasoning, multimodal context, and SLM efficiency for narrow workloads will dominate enterprise GenAI by 2027. The architectural pattern: large foundation models for reasoning surface, SLMs for high-volume execution, multimodal capabilities for cross-channel customer interactions.

Continuous learning systems with regulatory approval. The FDA's emerging framework for continuously-learning AI in medical devices (and parallel developments in EU AI Act, financial services regulation) will determine whether AI systems can improve from production data without retraining and re-approval cycles. Resolution of this question affects deployment economics significantly.

Industry-specific foundation models. The proliferation of domain-tuned models (medical, legal, financial, scientific) shifts the build-vs-buy economics. Most enterprises will adopt rather than build domain models, focusing internal investment on integration, customization, and operations.

AI governance frameworks become operational requirements. Companies deploying GenAI at scale need AI governance frameworks now — risk taxonomies, model risk management, ongoing monitoring, incident response, ethical review processes. This is engineering work, not just policy work, and it's where most enterprise GenAI programs will spend their next round of investment.

A glimpse into the future of generative AI

The GenAI landscape in 2026 is fundamentally different from 2024 — capability has expanded, costs have dropped, deployment patterns have matured, regulatory landscape has clarified. The companies leading in their industries by 2027 will be the ones investing now in disciplined GenAI deployment: clear use cases, the right architectural patterns, operational discipline, governance frameworks built into the operating model.

The risk isn't moving too fast. The risk is moving without discipline — investing in trends that don't apply to your workload, scoping for capability rather than compliance, treating GenAI as a project rather than an operating capability. The trends mapped above are real, but they only matter when matched against actual business priorities and capital constraints.

Ready to evaluate GenAI investment for your organization? Run the Project Estimator for a deterministic ballpark across implementation paths, or book a 45-minute Discovery with our GenAI engineers — we'll review your priorities, validate workload fit, and tell you honestly which trends should shape your 2026 capital allocation and which to monitor.

Talk to the team behind this

Building something like this in production?

Our senior engineers ship this kind of work for real teams. 45-minute call, no pitch deck — just architecture, trade-offs, and whether we're the right fit for your problem.